by WaMediaYBBTest | May 19, 2022 | Blog

By now, we’ve all heard more than we probably want to about the No Surprises Act and Good Faith Estimates. But there is another part to the whole Consolidated Appropriations Act puzzle that concerns mental health professionals.

Consolid…what?

What we think of as the “No Surprises Act” is not a law unto itself. No Surprises, along with several other healthcare provisions that will affect practices in the years to come, was bundled into a huge spending bill passed on December 21, 2020, titled the Consolidated Appropriations Act.

An interesting factoid, courtesy of the Senate Historical office: The CAA is the longest bill ever passed by Congress, to date. It tops out at 5,593 pages.

I wonder how many members of Congress actually read all 5,593 pages …

This blog concerns the tightening of provider directory regulations.

There are regulations for provider directories? Really?

Yep. And they aren’t new, either.

As of January 1, 2016, CMS became legally authorized to fine Medicare Advantage plans up to $25,000 per beneficiary if the number of errors in network provider directories exceeded a certain threshold. It doesn’t take a math major to realize that even 50% of this penalty would be a huge chunk of change out of a health insurer’s pockets.

The effect on practitioners began slowly, without much notice or fanfare. You’ve all been subjected to it, probably without ever realizing why (other than to moan about what an annoying pain in the rear it is). Services like CAQH, Availity, and the insurance payers themselves began sending around emails: VERIFY YOUR DIRECTORY ENTRY NOW.

Later, those same emails started to become more nagging, almost threatening, in tone: YOUR QUARTERLY ATTESTATION IS NOW DUE. ACT NOW TO AVOID DIRECTORY REMOVAL.

And. They. Just. Kept. On. Coming. From everyone.

YOUR DIRECTORY ATTESTATION IS DUE IN 10 DAYS. 5 DAYS. NOW. OVERDUE. ACT NOW TO AVOID BEING REMOVED FROM PAYER DIRECTORIES.

Wait, what? They can do that?

Yep.

Prior to January 1, 2022, directory suppression of providers who did not re-attest was at the discretion of the health plan. To my knowledge, most plans never suppressed names. The only plan that I have encountered which did, was United Healthcare.

At least on the national level. Some states (California, for one) did have stricter requirements prior to the Consolidated Appropriations Act.

But as of January 1, 2022, the No Surprises Act mandates:

- Health plans must refund enrollees the additional costs for out of network care if they paid an out of network bill for services & can show they went out of network because of inaccurate plan directories. Yes … Really!

- Health plans must pay an out of network claim with in-network level cost-sharing, if the patient saw an out of network provider due to a directory error. I would imagine that the patient would have to do some serious advocacy on their own behalf, though.

- In this event (an out-of-date directory) the out of network provider must not bill the patient more than the in-network cost-sharing. No balance-billing.

- Providers can require health plans to remove them from the directory at the time they terminate their contract.

- Health plans must have a regular method of verifying provider directory information.

- Payers must update their directory within 2 business days of receiving new information.

- Payers must confirm with providers every 90 days to re-verify accuracy of information.

- Payers must suppress provider information from directories if attestations aren’t received every 90 days. (Note: suppression does not affect claims for ongoing patients. Those will still be paid at the in-network rate. It’s the online directories that will not list your name. Maybe you don’t care …. But if an existing patient changes insurance, only to consult their new directory and discover that you are no longer listed…then what?)

Certainly, the need for accurate directories is important. Nor would verifying, or attesting, be a huge problem on the provider side, if a way existed for providers to go one place once per quarter and disseminate the same information to all plans. (Wasn’t that the original point of CAQH?) The burden comes with having to go multiple places online to provide the same information, take phone calls, fax or email forms. It’s a burden even for providers who have staff – because employees must be paid. This is employee time that could be devoted to patient care or billing.

Further reading, if you’re so inclined…

https://www.cms.gov/files/document/a274577-1b-training-2nsa-disclosure-continuity-care-directoriesfinal-508.pdf

https://khn.org/news/health-exchange-medicare-advantage-plans-must-keep-updated-doctor-directories-in-2016/

by WaMediaYBBTest | May 19, 2022 | Blog

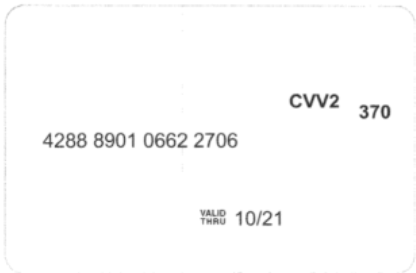

Transaction #: 123456789

Card Value: $1,500.00

Date: April 1, 2021

When I see this…

- Why should the clinician have to pay to be paid?

- Why do doctors have to spend time manually entering all these – there’s not even a QR code or a way to swipe them! Time is money too!

- How much do you want to bet that the insurance company and Mastercard/Visa are splitting that merchant fee as a “kickback?”

- They are making me log onto 10,000 different websites to get my remittance information for posting, rather than sending it to me in the mail or via my clearinghouse/software! That is SUCH a waste of my time.

- They’re saving themselves time and money, at the doctor’s expense!

- Payers know the doctors don’t have time to figure out these complex enrollments, so they count on people giving up and charging the virtual cards – and they are right.

NO … I’m not opinionated or anything…

Since 2014 when I received the first “Virtual Credit Card” (yes….it really WAS that long ago), the number of payments received in this format has proliferated like, well …..Tribbles.

It used to just be an annoyance, but all you had to do was call and they’d (grudgingly) send you a check.

Now, here’s what happens:

- Plans will refuse to allow enrollment in automated remits (ERA) unless the provider agrees to accept VCC or direct deposit, often from third-party intermediaries.

- Often the direct deposit option requires a fee also, which currently can be as high as 2.5%.

- Some plans refuse to pay by check at all. It’s either direct deposit or virtual card. Even if you’re out of network, out of area, or you only do business with them once every 5 years. Doesn’t matter.

- If they do agree to pay by check…it can take the check months to arrive, after several phone calls to follow up.

- The direct deposit registration process is often handled by third-party intermediaries and is incredibly complex and takes months. Which, frankly, I don’t understand. I go to my power company’s website and pay my bill in under 5 minutes simply by entering my routing & account #’s. So why does direct deposit registration with payers take months?

Now that I’ve raised your blood pressure to stroke levels….I have amazing news! We have won a victory over this abuse.

No way, really????

I know, right? Here’s how we fight these virtual cards and unreasonable-fee intermediaries:

On March 22, 2022, CMS quietly issued the following two guidance letters. In dry HIPAA-ese, they upheld providers’ rights.

For Health Plans: https://www.cms.gov/files/document/guidance-letter-vcc-eft-era.pdf

For Health plan vendors/business associates: https://www.cms.gov/files/document/guidance-letter-business-associate.pdf

Help! Is there an English version? I clicked the links, but what does all this gobbledygook mean? What do I need to do?

(Click here for the explanation and permanent solution to this pernicious skimming away of your hard-earned reimbursements.)

by WaMediaYBBTest | May 19, 2022 | Blog

Trying to figure out how to get paid for telehealth? *

*Doing audio-only? Coding and policies for audio-only telehealth are different. This blog focuses only on two-way audio/video telehealth.

If you thought it was bad in 2021, when you just had to deal with whether to use Place of Service (POS) 02 versus 11, and modifier -GT versus -95, now there’s a new complication.

Announced by CMS on October 13, 2021, the new place of service code (POS) for telehealth is 10, and it indicates telehealth when the patient is receiving services at home. Meanwhile, POS 02 has been shifted to denote that the patient is somewhere other than at home.

Don’t ask me why they felt it was necessary to make this distinction…

Next year, there will be a place of service for the bathroom.

When announcing the new POS 10, CMS originally stated that the implementation date for Medicare was April 4, 2022. However, the renewal of the Public Health Emergency (PHE) on April 13, 2022, trumps Medicare’s implementation of POS 10, because, according to the emergency waivers issued at the start of the COVID-19 pandemic, the telehealth flexibilities put in place as of March 6, 2020, will last until the end of the PHE (currently set for July 15, 2022).

Therefore, until the declared end of the PHE, coding telehealth for Medicare is still POS 11 (or whatever POS you would have used prior to the pandemic), plus modifier -95. This also applies to Medicare Advantage and Dual (Medicare + Medicaid) commercial plans.

Note: Medicare will pay for POS 10 (and 02) during the PHE, but coding POS 02 or 10 will impose a rate reduction.

This is because according to pre-pandemic Medicare telehealth policy, telehealth was subject to fee reductions. Medicare instituted the COVID telehealth billing flexibilities so as not to have to reprogram their payment systems, and also to ensure that healthcare providers could stay in business – sort of an important consideration during a worldwide pandemic.

What about commercial payers?

That’s the problem. Unlike Medicare and other government payers for whom billing instructions are a matter of public record, private payers don’t always openly disclose what they expect regarding telehealth coding – or they do, but it is often unclear, incomplete, and/or they make it so hard to find that it takes hours of searching.

Why is this so difficult? I just want to know how I can get paid for telehealth! Why can’t they all agree on how to bill it?

If I had the answer and solution to this problem, I would be able retire to Bora Bora tomorrow and you would have to find another Billing Buddy.

It’s frustrating, but right now everything depends on the payer and the policies they have implemented with regard to billing for telehealth. Some payers simply follow the lead of CMS. Others do their own thing…and they aren’t always consistent about it, either.

Your Billing Buddy’s recommendations for commercial payers:

- Check the payer’s website to see what (if any) instructions exist regarding billing for telehealth. I typically start by looking at the links marked “COVID-19” and then clicking around randomly until I get to information about telehealth and, hopefully, information about how to bill it.

- If you DO find something definitive, print it out. This will give you a snapshot of the date you obtained the information. Save it – you never know when you might need it in case of a clawback / recoupment attempt.

- Maintain a log or spreadsheet of the telehealth billing policy / coding requirements of the payers you bill most often.

- If you have time, feel free to call the payer, just don’t be surprised if it takes you a long time on the phone and at the end of the call you are more frustrated (but no more enlightened) than you were an hour or two previously.

- Subscribe to payer newsletters, blogs, and watch for webinars and trainings they offer.

- When in doubt, stick with POS 02 as long as the PHE remains in effect.

- If am unsure whether POS 10 is acceptable yet, but think it appropriate to try, I send in one test claim. I make note on my spreadsheet of the patient account #, date of service, and date submitted. Then, before submitting any more, I wait until it is adjudicated. Once I have my answer, I correct and release the remainder of claims that I have put on hold. That way, if the claim does get denied or underpaid, a single claim can be corrected quietly, without a large number of claims needing correction.